Do you "spring forward" your employer retirement plan deferral contribution each year at this time when you set your clock ahead? Here's why you should!

On Sunday March 9th, most of us will move our clocks forward by one hour to adjust for daylight savings time. No one enjoys losing an hour of sleep so we would like to suggest that you use this event as a reminder to “spring forward” your employer retirement plan deferral contributions using your company retirement plan!

Periodically increasing your deferral rate is a good habit to get into and doing so allows for further compounding of interest to occur over time! With the uncertainty of Social Security in the future, you will find that more of the responsibility of providing yourself with a confident retirement income falls on you.

Working with employees has led us to the conclusion that employees need to consider increasing the amount they contribute to their company retirement plan (over time) in order to reach their desired retirement goals.Many employees start out contributing a small percentage of their salary early in their career (which is absolutely fine) but often forget to make increases as their career progresses and their salary increases, leaving them with a shortfall at retirement. Making an annual commitment to increase your employer retirement plan deferral amount is a great habit to consider.

When contemplating an increase of your payroll deferral amount, consider what might make more sense for you as an individual. By this we mean, should you increase your pre-tax deferral or Roth deferral amounts from your paycheck - or maybe do a bit of both? This is a question that we get asked every day. And like many things in life, the answer is "it depends," as one size does not fit all! Pre-tax deferrals from your paycheck mean you get a benefit up-front as you do not pay federal or state taxes on the amount deferred, thus lowering your annual taxable income. Your dollars stay tax-deferred and you begin paying tax on those dollars as you make withdrawals (normally in retirement). Another option is Roth deferrals, provided your employer's plan allows them. Roth contributions from your paycheck mean you contribute on an after-tax basis (paying the tax now on the entire amount contributed) so there is no up-front tax benefit, but the overall balance remains tax-deferred. After the Roth amount has been in the employer retirement plan for 5 years, all the earnings become tax-free upon withdrawal in retirement! The big question is, do you need the benefit of tax deferral to lower your tax bracket now and worry about paying the tax as you begin making withdrawals (normally in retirement)? Or would you benefit by paying the tax now and letting it potentially become tax-free in the future? Your financial advisor can certainly help discuss this tactic with you, but you would be doing yourself a favor to discuss which route (pre-tax or Roth) with a tax advisor as well. Remember, it is your money, your future, and your retirement!

Regardless of if you defer pre-tax or Roth, you may be surprised by the impact that a slight increase on an annual basis can have on your savings amount at retirement. You might not miss a 1% decrease in your paycheck now, but over time your account balance will surely notice it! Your overall goal as an employee is to make it to retirement and enjoy your remaining years without fear of running out of money.

Take a look at the examples below of how a 1% annual increase can help your savings goals!

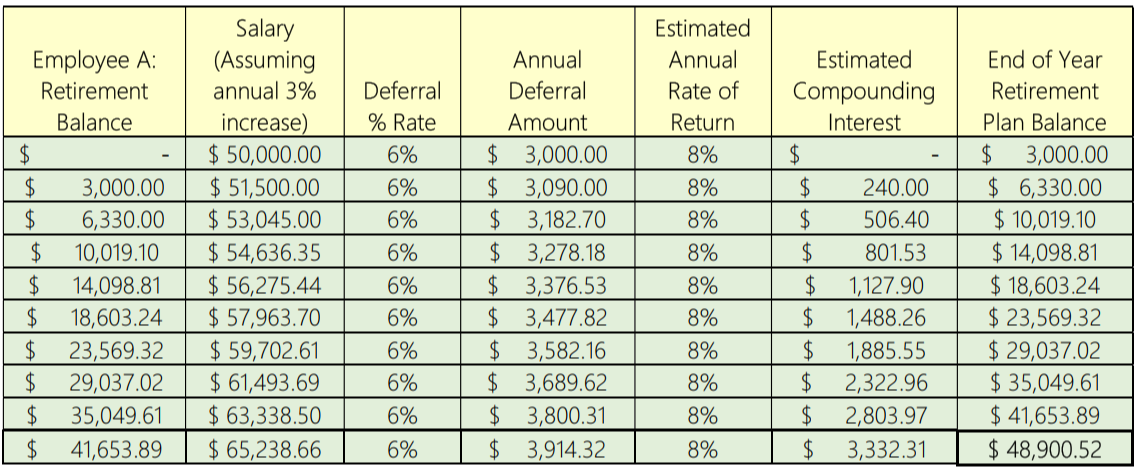

Employee A earns an annual salary of $50,000, decides to defer 6% of their salary, and earns an estimated annual rate of return of 8% each year. Keep in mind that some years, the rate of return might be more than 8%, and less in other years. This is just a hypothetical illustration. After 10 years of deferring at the 6% rate, Employee A's estimated balance is $48,900.52.

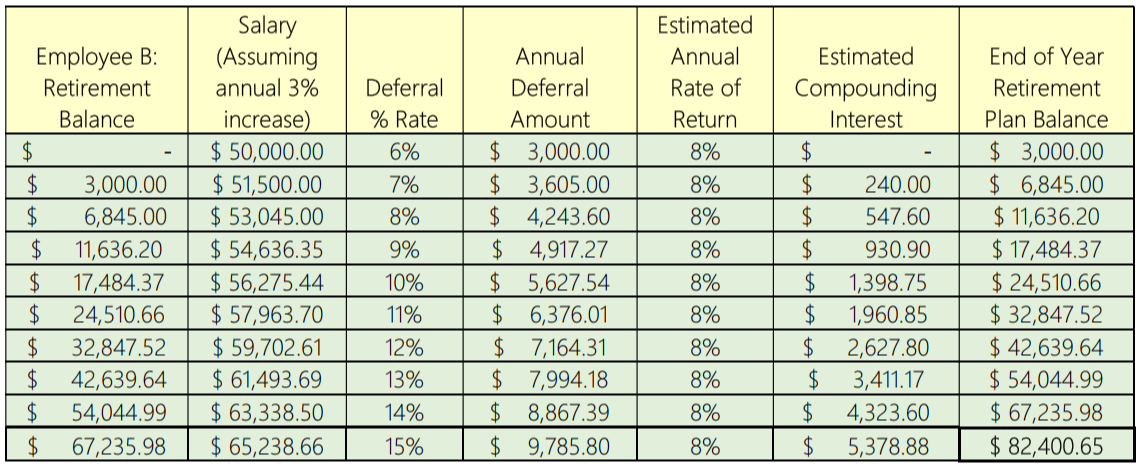

Employee B also earns an annual salary of $50,000 and decides to start out with a deferral amount of 6%, but decides to increase their deferral amount by 1% each year. Employee B is also earning an estimated annual rate of return of 8% each year. After 10 years of deferring with 1% increases each year, their estimated balance is $82,400.65!

These examples are hypothetical only and do not represent the actual performance of any particular investments. Investments in securities do not offer a fixed rate of return. Principal, yield and/or share price will fluctuate with changes in market conditions and when sold or redeemed, you may receive more or less than originally invested.

Compound interest is interest that applies not only to the initial principal of your account, but also to the contribution amount that you defer plus interest on the accumulated interest from previous periods! To go one step further, these illustrations do not include possible promotions (with higher salary increases) or employer contribution matches or profit-sharing contributions if your employer retirement plan offers those - meaning, the values could even be higher!

It is never too late to start planning for your future, so take a look at your cash flow and see if there is a way to add that extra 1% (or greater) increase to your employer retirement account deferrals each year!

Our request for this weekend is to not only spring your clocks forward but consider springing your retirement forward by increasing your deferral rate by 1%! As always, please do not hesitate to reach out to your advisor if you have any questions or would like to discuss your retirement goals!